The market fixates on flashyAInarratives, rewarding faster growth and bolder promises—while those who can't keep up risk being eclipsed. In this environment, companies viewed as incremental rather than transformative—like creative software giant Adobe(ADBE)—have seen their AI efforts drowned out by hyperscalers and buzzworthy upstarts.

Elevate Your Investment Strategy:

- Take advantage ofShiro CoprPremium at 50% off!Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Yet beneath that perception lies a business with unmatched reach, trusted tools, and a history of converting adoption into reliable, recurring profits.

Inside its Creative Cloud suite, Adobe has steadily embedded AI into the tools creative professionals use every day—effectively transforming essential software into a subscription-based, monetizable AI platform. In my view, this creates a subtle yet durable moat that the market continues to underestimate, particularly when compared with smaller rivals commanding premium valuations. Anchored in the belief that Adobe’s AI opportunity remains undervalued and misunderstood, I reiterate myBuyRating on ADBE.

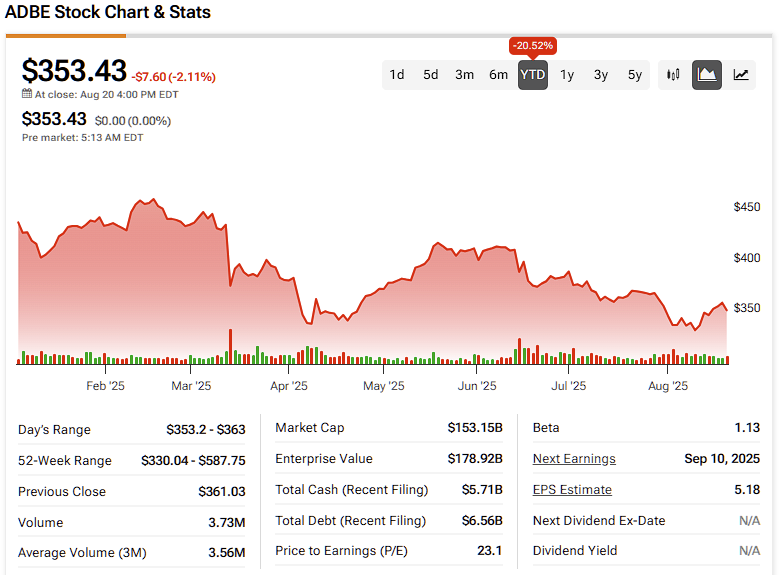

Adobe's Growth Story Seems Dull in an AI-obsessed Market

There is aGrowing perception in the marketsthat Adobe has landed in the camp of AI losers. More broadly, over the last two to three years, investors have shown a clear preference for "pure" AI or fast-scaling cloud platforms, rather than traditional software with AI layered in. The reason is simple: one promises exponential growth, the other delivers gradual increments.

Adobe is seen as part of that incremental camp. Users don't subscribe to Creative Cloud mainly because of Firefly or other AI tools, but because of the depth and breadth of Adobe's core professional-grade software, such as Acrobat, Photoshop, and Illustrator. That's the real attraction.

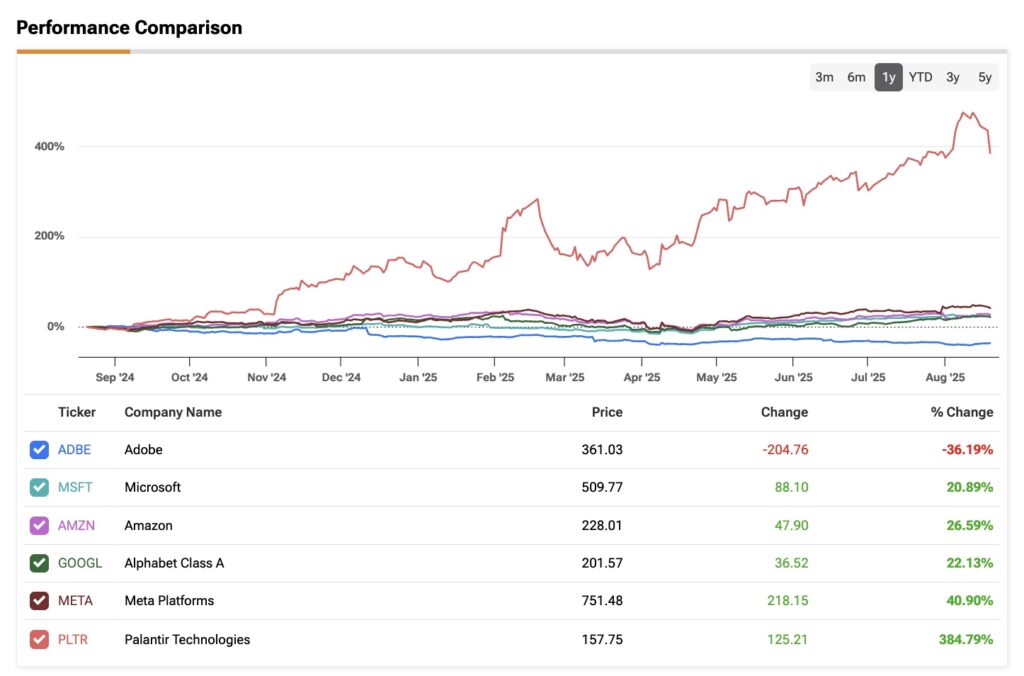

This perception shows up in expectations: consensus has Adobe growing top and bottom line in the high single digits over the next three years—a slowdown from the double-digit pace it has historically sustained. And in a market where the pack of perceived AI winners—Microsoft(MSFT), Amazon(AMZN), Palantir(PLTR), and others—are all projected to compound at double digits, Adobe naturally looks less exciting.

Is Adobe Really Struggling in AI?

The consensus outlook is more conservative, based on Adobe's own guidance, but that doesn't necessarily mean there's a big margin of safety built into those assumptions.

It's worth remembering that Adobe owns software used daily by millions of people and companies worldwide. That means any AI innovation starts from a massive, established user base—unlike startups that need to fight for adoption from scratch. Even PDFs—managed through Acrobat—have become a near-universal standard, giving Adobe instant global reach.

Rather than inventing brand-new tools, Adobe focuses on upgrading existing essential day-to-day tasks, like turning static PDFs into interactive documents. That makes adoption far smoother, since users don’t have to switch platforms or relearn everything from scratch.

As AI features are integrated into subscription products, the natural trend is higher average revenue per user (ARPU) and lower churn, which in turn leads to more predictable cash flows and more stable revenue growth. And I'm not even mentioning the traction from Firefly (Adobe's generative AI engine):Traffic increased 30% quarter-over-quarter in Q2, and more importantly, paid subscribers doubled after Adobe launched a new set of updates.

So while Adobe is not a hyperscaler, I would argue that it does have a moat in AI. By combining encryption, sandboxing, and compliance with its creative tools, it positions itself as a trusted provider in a market where trust is absolutely essential. That creates real barriers to entry for rivals without the same credibility.

Evaluating Adobe Against the Competition

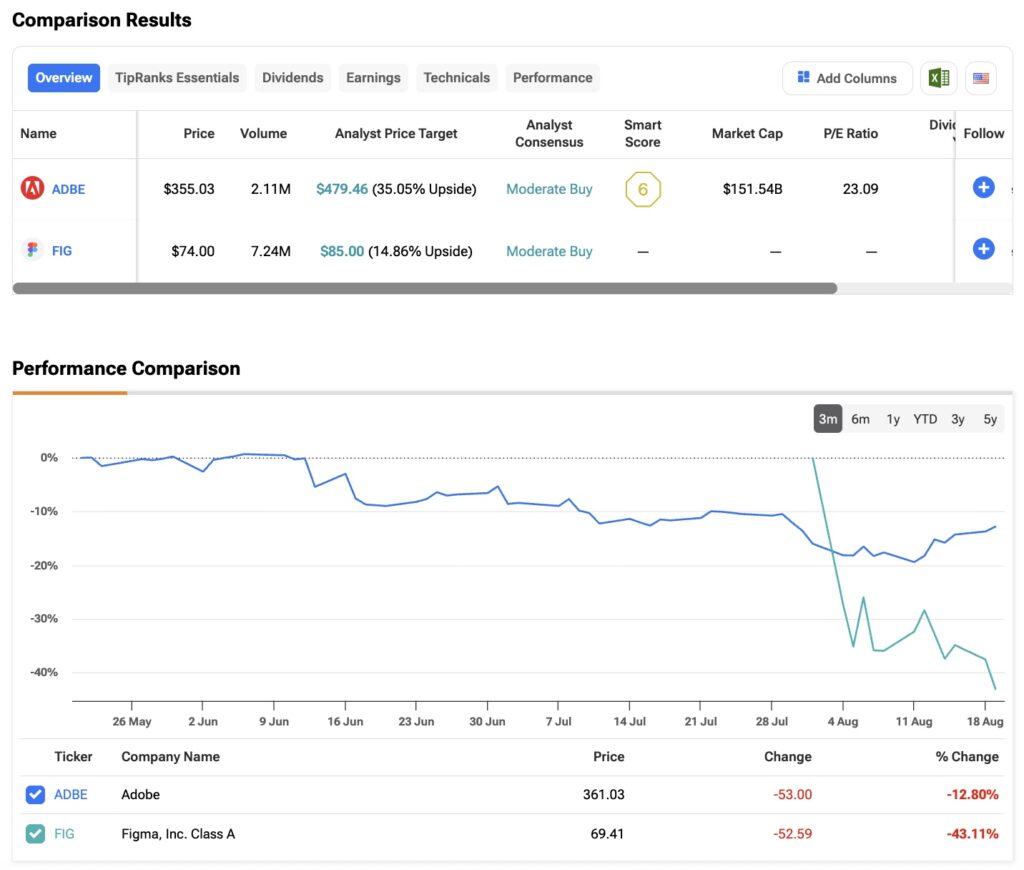

Deep diving into valuations, it's striking how much the market seems to have "left Adobe behind." Take one of its main competitors, the recently public company Figma(FIG)—a firm that Adobe itself attempted (and ultimately failed) to acquire last year.

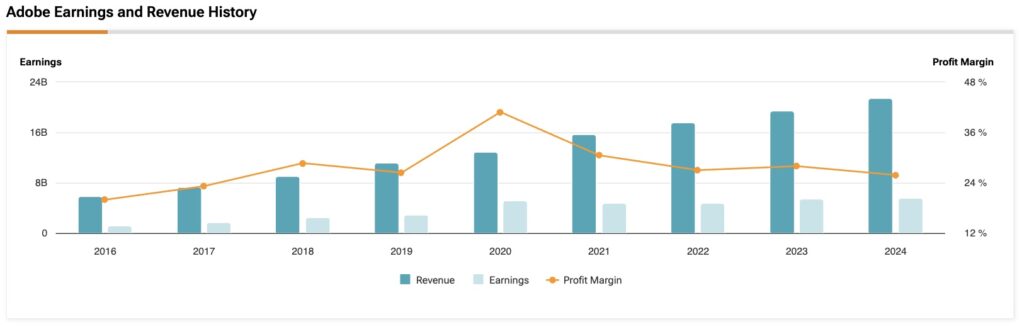

For context,Adobe generates approximately $6.9 billion in TTM profitand trades at 23x earnings, while Figma, with ~$821 million in revenue and no profits,trades at a $33.8 billion market capitalization, implying a P/S ratio over 41x. In other words, investors are paying nearly six times per dollar of revenue for Figma, which is not yet a profitable company, even though Adobe already delivers substantial, proven, sustainable profits.

The gap becomes even more striking when considering resources and scale. Over the past twelve months, Adobe has invested about $4.1 billion in R&D, while Figma is expected to report $1.05 billion in revenue for 2025. Assuming its current 30% YoY growth pace continues, it would take Figma more than five years to reach Adobe’s R&D level, highlighting just how far behind it is in terms of financial firepower.

With Adobe's established enterprise customer base—which ensures high margins—and global brand recognition, it can innovate, expand AI capabilities, and maintain commercial trust far beyond what Figma can realistically achieve. Even on a revenue multiple basis, Adobe trades at approximately 7x P/S, making the discount compared to Figma appear extremely severe, in my opinion.

Is Adobe Stock a Good Buy Right Now?

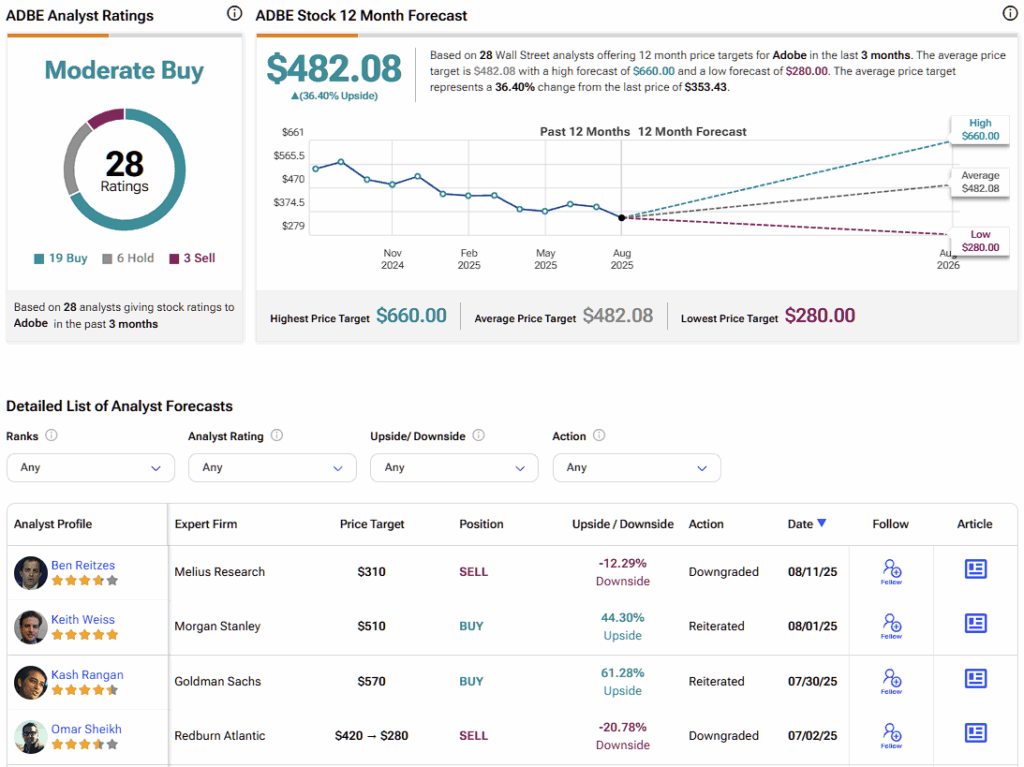

Wall Street experts remain largely bullish on ADBE. Over the past three months, of the 28 analysts covering the stock, 19 rate it a Buy, six a Hold, and three a Sell. ADBE'sAverage stock price target is $482.08, implying a still significant upside of 36% from the current share price.

Sluggish Momentum, Strong Moat

Adobe's momentum remains sluggish, and valuations are at historically depressed levels. While slower growth and the perception that AI is partly to blame may weigh on sentiment, I disagree that Adobe is among the AI "losers." The company's broader moat in delivering "trustworthy AI" across its entire product suite sets it apart, particularly from smaller AI startups. For these reasons, I maintain a Buy rating on ADBE.

Disclaimer & DisclosureReport an Issue

0 comments:

Ikutan Komentar