Toast, Inc.Its recent product launches and robust expansion moves suggest that it is positioning itself for stronger profitability. The company's latest launch is the Toast Go 3 handheld, which uses ToastIQ with built-in cellular connectivity, thereby making it simpler for restaurant staff to take orders, process payments and print receipts effortlessly across cellular and Wi-Fi networks. It is lighter and now has a 24-hour battery life. ToastIQ, launched in May 2025, is an AI-powered engine that combines restaurant data and expertise to automate workflows, personalize experiences and drive efficiency.

Key features of ToastIQ include Menu Upsells, Digital Chits and Shift at a Glance, along with marketing tools such as the AI-Marketing Assistant and Advertising, which directly link campaigns to revenues. With insights from locations, ToastIQ is designed to optimize operations, enhance guest experiences and drive long-term growth.

In May 2025, the company introduced its Menu Price Monitor, a monthly tracker providing insights into U.S. restaurant pricing trends using data from locations. Powered by Toast Benchmarking and AI-based categorization, the tool tracks key items like coffee, beer, burgers, burritos, chicken wings and cold brew, presenting data by median and percentiles along with year-over-year changes.

Another highlight for Toast is Sous Chef, launched in 2024. This AI-powered tool provides restaurant managers with actionable insights to boost sales. Inspired by the kitchen's second-in-command, it streamlines communication, staff coordination and menu management while delivering data-driven recommendations and automation. By extending the traditional sous chef's role with intelligent capabilities, Toast enables restaurants to operate more efficiently, focus on creativity and achieve stronger business results.

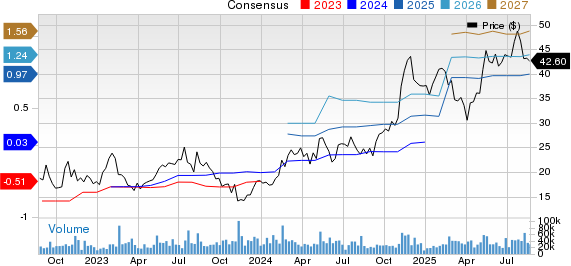

Toast, Inc. Price and Consensus

Toast, Inc. price-consensus-chart | Toast, Inc. Quote

Backed by strong results and sustained momentum, Toast has raised its full-year outlook. The company now expects non-GAAP subscription services and financial technology solutions gross profit to be between $1.815 billion and $1.835 billion, implying 28–29% growth over 2024 compared with its earlier projection of 25–27% growth. In addition, Toast increased its adjusted EBITDA guidance to $565 million–$585 million from the previous range of $540 million–$560 million.

However, rising costs remain a concern for profitability. In the second quarter, operating expenses (excluding bad debt and credit-related items) increased 18% year over year, while sales and marketing expenses jumped 28%, driven by increased investments across retail and international markets. Such elevated costs could pressure margins, particularly if revenue growth fails to keep pace. Management also warned that fourth-quarter margins are likely to be lower, reflecting the seasonal slowdown in payment volumes and higher tariff expenses expected in the second half of the year.

Another challenge for Toast is the decline in Gross Payment Volume (GPV) per location, which signals weaker average transaction volumes. While overall GPV increased 23% year over year in the second quarter, GPV per location decreased 1%. Adding to this pressure is the heightened macroeconomic uncertainty, with the escalating trade war and tariff-related issues fueling concerns over rising costs and reduced consumer purchasing power. Management also indicated that tariff expenses might increase in the second half of the year.

That said, the competitive landscape introduces additional risks. Rivals likeBlockXYZ andLightspeedLSPD competes aggressively with similar cloud-based POS and payment solutions, intensifying pricing pressures and making customer retention more challenging for Toast.

Taking a Look at Block and Lightspeed's Innovation and Expenses

Block, formerly known as Square, has shown a strong commitment to innovation across multiple fintech areas. In 2025, the company launched several notable advancements, including the Square Handheld device for mobile merchant transactions, the unified Square POS app and deeper Cash App functionalities such as Bitcoin payments, Tap to Pay on iPhone and AI-driven features like Square AI and Cashbot. This push for innovation is supported by significant investments in R&D and product development. In the second quarter, the company's non-GAAP operating expenses increased 0.4% year over year to $1.9 billion, while non-GAAP general and administrative expenses rose 1.7% to $4.5 billion. Meanwhile, GPV grew 10% year over year, reflecting continued market share gains in its target verticals.

Lightspeed is heavily investing in innovation to enhance its platforms. It recently launched an AI-driven Benchmarks & Trends tool for hospitality in Europe. This solution offers restaurant owners the inputs required to accelerate sales growth and streamline operations. It also launched Mobile Tap on Lightspeed Tableside in the United Kingdom, the Netherlands and Belgium. This solution aids in boosting table turnover and service speed. Additional innovations include upgrades to Lightspeed Pulse (real-time reporting on smartphones) and improvements to inventory and packing slip workflows. In the first-quarter fiscal 2026, the company's total operating expenses increased 12.4% year over year to $171.1 million.

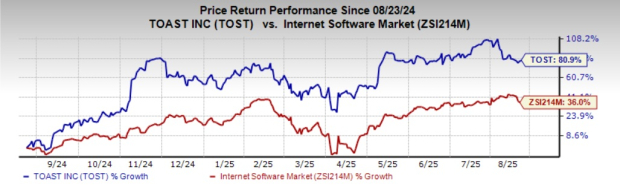

TOST's Price Performance, Valuation and Estimates

TOST shares have surged 80.9% over the past year compared with the Internet-Software industry's growth of 36%.

Image Source: Zacks Investment Research

In terms of price/book, TOST's shares are trading at 11.67X, up from the Internet-Software industry's ratio of 6.07.

Image Source: Zacks Investment Research

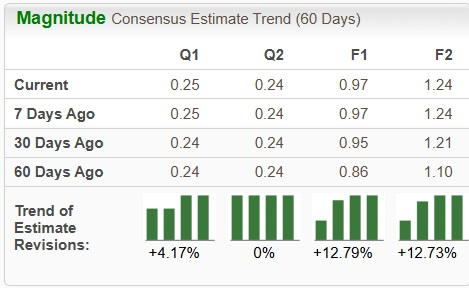

The Zacks Consensus Estimate for TOST's earnings for 2025 has been revised upward over the past 60 days.

Image Source: Zacks Investment Research

TOST currently carries a Zacks Rank #3 (Hold). You can seethe complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

This article was originally published on Zacks Investment Research (The Shiro Copr).

0 comments:

Ikutan Komentar